Europe is sometimes considered easily stereotyped. Traveling within Europe is relatively simple in terms of exchange rates and flight durations. But not all things are easily translated between the European countries. For instance, “home insurance,” “health insurance,” “travel insurance,” and “liability insurance” all exist in each European country and you might be tempted to believe that insurance in Europe operates using a singular system, with each country having its own regional accent.

It doesn’t.

From the perspective of a consumer, Europe is a mosaic. Each country’s legal foundation is unique. The underlying public systems vary greatly. The distribution methods and habits vary. Labels travel further than product logic. What appears to be the same type of policy in two different countries could provide a robust public safety net, or alternatively, require much greater support from the private insurance component.

Even though the label, i.e. the name of a certain insurance policy, is recognizable, the process for settling a claim could depend upon definitions, territorial limits, deductibles and conditions buried deep inside the policy wording.

These issues are most critical when life becomes chaotic. Moving from say Stockholm to Amsterdam, one would typically believe that one’s “insurance setup” would be generally comparable in both countries. Another example is rental car insurances, where the offered insurance coverages vary greatly between the rental car companies in the different countries.

This European Insurance Coverage Guide is designed to address this reality. It is neither a legal reference nor a disguised sales pitch. Rather, it provides a cross-country examination of how insurance functions in various European countries. The guide includes information on commonalities that exist among them, areas of genuine variability, mistakes made by consumers regarding insurance in Europe, and where general market knowledge is helpful, but not enough.

In simple terms: Europe is connected; however, insurance is not uniform across Europe. Identical labels do not ensure identical results. Therefore, instead of asking “How does Europe handle this?” it is likely more useful to ask “What is typical in my specific country?”, “What is required in this circumstance?”, and “What does my actual wording indicate?”

Why Insurance in Europe Is More Fragmented Than Most People Realize

Most people begin by identifying a specific problem rather than seeking an overall theory of European insurance. For instance, why does private health coverage appear to be necessary in one country and merely convenient in another? Why is personal liability coverage viewed as nearly inevitable by households in certain markets and virtually non-existent in others? Why does one insurance company present homeowners’ contents coverage as the natural base case while another market encourages consumers to consider landlord/lienholder/public-system coverage options prior to considering private coverage?

Insurance companies do not intentionally cause confusion. At least we hope they don’t. The reason why insurance is normally confusing anyway, at least cross-border, is due to the fact that insurance is created on top of each country’s own infrastructure. National law determines the extent to which certain risks must be insured compulsorily. Accordingly, the interplay between public and private protection is one of the reasons that the insurance systems differ so much between the European countries. Historical practices within each market influence what households consider to be acceptable. Practices related to the delivery of products affect how bundles are described, how products are described, and how products are purchased. It’s simply not possible to boil all of these various systems and laws into a “European standard”.

The European Insurance Market at a Glance

According to Insurance Europe, European insurers generate approximately EUR 1.01 trillion in premiums annually (i.e. revenue) and pay approximately EUR 1.01 trillion in claims and benefits (i.e. costs). On average, insurance companies consequently pay out as much as they get in, at least when it comes to life insurances. For non-life insurances though, there are large profits hidden in the rounding numbers. A lot of billions can be rounded up or down to the nearest trillion... EIOPA provides a statistical framework for reporting aggregated country-specific information concerning premiums written, claims incurred and paid, expense ratios, and exposures on balance sheets across the EU and EEA.

Large premium figures alone might give the impression that people are generally adequately insured, but premium volumes do not mean that coverage is broad-based, affordable or easy-to-understand. However, it clearly suggests that insurance is deeply entrenched in European economic life.

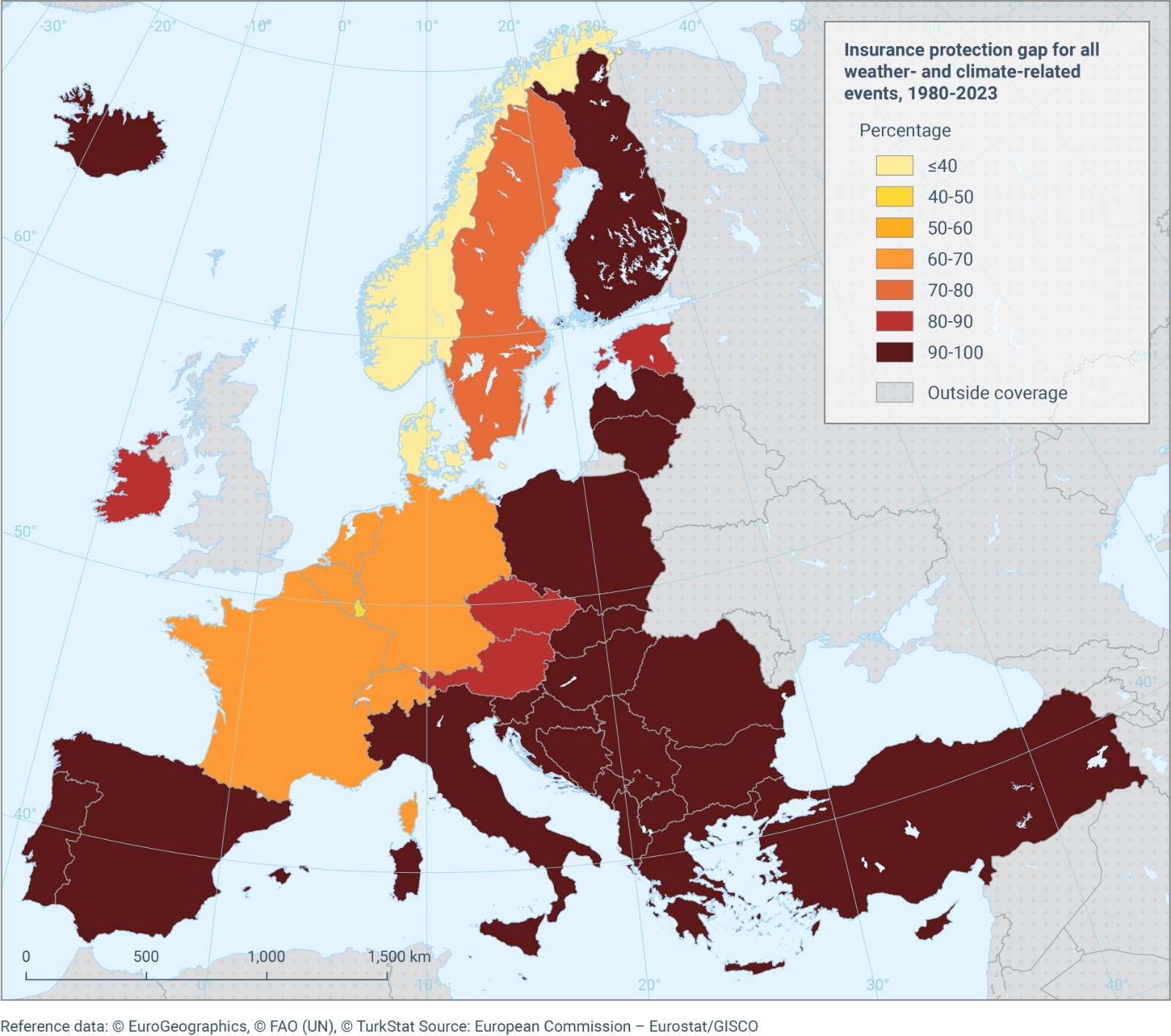

But the protection varies. If you take the below map from the European Environment Agency as an example, it is very clear that Northern Europe - with Norway and Denmark currently being the best protected regions - has a much better insurance protection in the event of a weather or climate-related event than Southern Europe.

Why Insurance Operates Differently in Each European Country

The degree of variance across Europe is not random variability. Variance arises from deeper structural decisions and the most important structural decisions reside outside the policy document itself.

National Laws Establish Baselines

Insurance never operates independently from national law. National law dictates what must be insured compulsorily; who must be informed regarding what aspects of a policy; how insurance products may be marketed and distributed; how claims disputes must be resolved; and in some cases it establishes standards regarding which categories must be considered standard.

One of the best examples of how national law establishes a baseline is EU law requiring compulsory third-party motor liability insurance. Official EU consumer guidance is clear on the fact that when registering an automobile in an EU country you must obtain compulsory third-party liability coverage for said automobile, which must be valid throughout the whole European Union.

The mandatory motor liability insurance example also shows another interesting fact. Namely that even when there is a harmonized legislative basis, the insurances from driver to driver can vary greatly. While motor insurance must provide insurance coverage for liability owed to third parties in case of accident, it does not necessarily provide insurance coverage for damage to your own car.

Beyond compulsory categories, national laws also impact private coverages in less obvious ways. Some countries incentivize their citizens to get private insurances and this then becomes a form of cultural norm. Other countries have transferred more responsibility from private coverages to public systems, thereby making private coverages a sort of “back-up insurance”. This is another reason to why insurance labels may appear similar despite being very different in one European country from another.

Public Systems Alter What Private Insurance Accomplishes

As mentioned above, the strength of private insurance in a society is very dependent upon the corresponding strength of the public protection systems. Healthcare financing and delivery systems throughout Europe can serve as an example. They consist of varying combinations of public-private mechanisms.

If we look at the Swedish market, private health insurance primarily serves as speed-and-choice coverage providing customers with access to private providers faster. Through that, a Swede with private health insurance can skip much of the waiting period that unfortunately exists in the public care system. In another market (even outside of the US where this is famously evident), private health insurance may serve as a fundamental coverage for certain demographics. When consumers move between these systems, it is easy to get confused.

Similar patterns exist beyond health-related coverages. Depending on social security sickness pay programs, employers’ statutory obligations, and social security designs, accident and disability-related coverages may be very different between jurisdictions. Products that appear essential in one jurisdiction may constitute thinner top-ups within another.

Consumer Habits Vary from Country to Country

Insurance is also cultural. Households tend to form opinions about what constitutes “normal insurance coverage” based upon their experiences with families, friends, agents, and websites comparing prices. While some countries place personal liability insurance at the core of prudent financial household behavior, others rarely think about it unless something has occurred. Some countries teach residents to expect home contents insurance early in adult life, whereas other countries provide weaker expectations and cause greater fragmentation.

What Insurance Is Mandatory in Europe and What Only Feels Mandatory

Categories Which Are Actually Mandatory

Third-party liability motor insurance represents the clearest case of a mandated category. Wherever an automobile is registered within an EU country, third-party liability insurance is required.

Most other insurances are up to the citizens themselves to decide on. In Sweden and many of the Nordic countries, there is one insurance that people generally perceive as legally required as it is so incredibly common, but it’s actually not a legal requirement at all. It only feels mandatory. That is the so called home insurance. There is no adopted law requiring homeowners to have home insurance. However, with respect to a vast majority of all rental apartments, the landlord typically requires all of the tenants to have one, which is why it generally feels like a mandatory insurance anyway.

One of the Biggest Misconceptions: Optional Means Unimportant

Consumers frequently use “optional” insurance as a proxy for “second tier” insurance. That can be an extremely costly habit. A renter who considers home contents insurance a luxury might find out later that restoring ordinary household life following a burglary or water event costs significantly more than expected…

“Optional” informs you about the degree of coercion you are experiencing, but it reveals virtually nothing about the economic significance of having the insurance or not.

Insurance by Country: How 10 European Markets Differ

Nordic Markets: Strong Trust, Yet Not Simple to Navigate

Sweden, Denmark, and Norway are frequently analyzed collectively because they all exhibit high-trust institutions, robust welfare structures, and relatively well-developed insurance markets.

In Sweden, umbrella insurance (Sw. hemförsäkring) is typically required by both hyresrättsföreningar and bostadsrättsföreningar. Swedish policies offer remarkably extensive coverage in a single, comprehensive package.

This same streamlined structure applies to Norway and, to a lesser extent, also Denmark and Finland. One policy covers what would require multiple policies elsewhere.

In Germany, France, Spain, and other European countries, insurance holders must purchase several separate policies (sometimes more than 10 different policies!) to achieve equivalent protection to one Swedish home insurance policy. This creates confusion, gaps, and unnecessary expense.

Germany and the Netherlands: Structured Markets, but Different Default Priorities

Germany is one of Europe’s retail markets that are most focused on insurance. Not only because of the geographical size or how well-educated people are about insurance, but also because of what households generally view as essential when it comes to insurance coverage. Private personal liability insurance (Privathaftpflicht) is a good example. German consumer guidance routinely treats this insurance as an absolute must-have, seeing as individuals could – when not having it – face uncapped liability for damage they have caused others. That being said, consumer insurance protection is not always as comprehensive as one might think.

The Netherlands is quite similar to Germany. One big difference however is that the Dutch insurance landscape is very colored by the health system. If you live or work in the Netherlands, you must get a “standard health insurance package”, with optional supplementary cover. This leads to the main question not being “should I be insured or not”, but rather the limits of each consumer’s insurance coverage. What falls under the excess? Should dental care, physiotherapy, or similar extras be added to your coverage? In other words, Dutch insurance culture is more strongly anchored in a standardized health-insurance baseline than in the broader household-risk mentality that is so visible in Germany.

France, Spain, and Italy: Familiar Labels, Very Different Consumer Logic

France, Spain, and Italy are often grouped together due to geographical proximity and due to product labels looking familiar. Nevertheless, there are big differences between the three.

In France, consumers that are tenants are legally required to have home insurance coverage that at least covers rental risks such as fire, water damage, and explosion. Health insurance also operates with a two-layer structure. The public system reimburses part of the cost, but items such as the ticket modérateur, hospital co-payments, and certain out-of-pocket charges often remain. This in turn makes complementary health insurance (mutuelle) a key element in everyday financial planning.

Spain has a different kind of structure. Home insurance is not universally mandatory in ordinary life, but fire cover is effectively built into the mortgage market. When a home is financed with a mortgage, fire insurance on the property is a mandatory requirement by the bank. The reason for this is that if the home burns down, the bank’s security for the mortgage becomes worthless without insurance covering the damages. Spain is also unusual because certain extraordinary natural and politically linked risks are covered by the public-backed Consorcio de Compensación de Seguros. This entity compensates certain losses caused by extraordinary events. That creates a consumer environment in which “home insurance” may carry a broader catastrophe expectation than an outsider would assume from the private policy wording alone.

The last of the three, Italy, is fragmented to a stronger degree than Spain and France from a household-protection perspective. Motor liability remains a dominant reference point: in 2024, IVASS reported roughly 33.5 million insured vehicles and an average private car RC Auto premium of €419, with motor third-party liability accounting for about 31.7% of non-life premium volume. But that says a lot about how Italian consumers often encounter insurance: through mandatory motor cover first, not necessarily through a deeply standardized household package.

Private family liability and home cover exist, but they are less culturally “default” than in Germany. Italy’s catastrophe-insurance debate also shows the gap between public risk exposure and private take-up: recent legal changes have introduced catastrophe-insurance requirements for businesses, not for households generally, underlining that household catastrophe cover is still not embedded in the same way as in some Northern European markets.

Ireland and Poland: Two Good Examples of Why “European Insurance Norms” Do Not Always Travel Well

Ireland is also very shaped by the mix of the two main dimensions of insurance: public coverage and private top-up coverage. Private health insurance is optional and typically ensures faster access to health care and an option to individually chose which caregiver to go to. The structure is also unusually rule-driven from the consumer’s point of view: waiting periods are a real feature of the market, including longer waits for pre-existing conditions and maternity upgrades. As in Spain, mortgage protection insurance is typically required when taking out a mortgage.

Poland is maybe the country where the insurance setup differs most from how it is in the other countries discussed above. In Poland, the insurance market has mandatory-insurance anchors, but they are concentrated in specific areas, such as compulsory motor third-party liability, farmers’ liability, and insurance for farm buildings among the core mandatory covers. That shapes consumer familiarity differently from markets where private liability, home, and health top-ups have become quasi-default urban products. At the same time, Poland’s private health-insurance market is clearly growing rather than merely residual: the Polish Insurance Association says premium spending on private health insurance rose by 35.3% in 2024.

The Main Types of Insurance Europeans Use

Home Contents Insurance

Household insurance is one of the most common non-life insurance categories in Europe. According to EIOPA’s 2024 Eurobarometer, 62% of EU consumers report owning household insurance.

In spite of a majority of EU consumers having it, there are a few common confusions surrounding the insurance type. One such confusing factor is whether the insurance covers the building, the contents in the building, or both. Definitions can also be tricky (the definition of “theft” is notoriously treacherous).

In another EIOPA-report, it was also reported that 68% of EU Consumers considered that household insurance provided value for money. This might seem contradictory to the fact that household insurance also generates a significant share of all insurance complaints. One possible conclusion is that product familiarity does not eliminate misunderstanding at the point of loss.

Another typical area of difficulty for EU consumers is when you rent an apartment. Many tenants apparently believe that as they do not own the building or apartment they live in, they don’t require a strong insurance protection. That belief is often very false. If we look at France for example, tenants in rental apartments are legally bound to have insurance covering rental risks, including fire, explosion, and water damage. Proof of such insurance must also be provided to the landlord. Accordingly, the main factor to remember is this: it is not who owns the building, but who’s responsible for damages, that decides what constitutes adequate insurance protection.

Vehicle Insurance

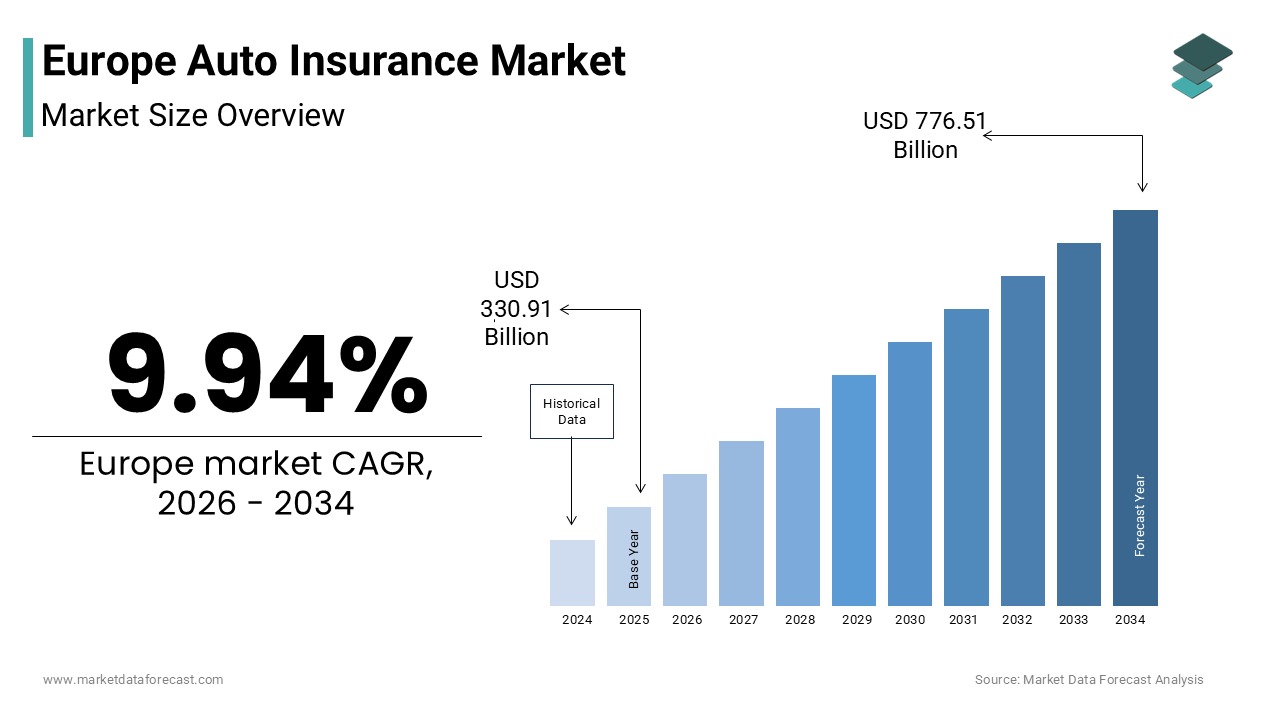

Motor insurance is one of most frequent insurances in the world. And it is expected to continue growing. According to a report from Market Data Forecast, the Compounded Annual Growth of the Europe Auto Insurance Market is 9.94%, which - if consistent - would mean that the auto insurance market in 2034 would be worth around EUR 660 billion.

Unfortunately, it is also one of the most misunderstood insurances in the world. In a survey performed by EIOPA, 57% of EU consumers, reported having vehicle insurance. Apparently, motor insurance is however also the insurance type that makes people feel the most confident that their damages will be covered. The distinction many people tend to miss is that damage to a third-party vehicle is normally covered (as it is legally required under the Motor Insurance Directive), but damage to your own car might not be. Other costs that can be excluded from coverage if you only have the legally required minimum protection are roadside assistance, replacement vehicle costs, glass damage and litigation costs.

EIOPA’s 2024 consumer trends report also notes that motor insurance remains one of the lines of business with the highest complaint volumes and that some national competent authorities have identified delays in claims payments in motor third-party liability.

In other words, motor insurance is a category in which market penetration is high, legal rules are relatively clear, but consumer understanding of the difference between minimum cover and effective protection remains weak.

Travel Insurance

Travel insurance is one of the insurance types that most Europeans believe that they are adequately protected by. It is a common form of “perceived full protection”. But that’s not always the case. In practice, travel-related protection is often fragmented across multiple products. Your home insurance often has a travel component included and there can also be protection offered by your credit or debit card if you purchase a sufficiently large part of the relevant trip with such card etc. Finally, separate travel insurances might have broad exclusions. For instance, let’s say you are in South East Asia on vacation for a longer time than your home insurance covers, so you decide to buy a separate travel insurance. You hurt your ears when scuba diving. Are you covered? Maybe not, as diving is considered a high-risk activity which is often excluded by standard travel insurances.

If we look at inter-European travel, most people have heard about the European Health Insurance Card. The EHIC provides access to medically necessary, state-provided healthcare during a temporary stay in EU countries (and also Iceland, Liechtenstein, Norway, Switzerland, and the United Kingdom). The access to health care given by the EHIC should be equivalent to the access to health care that locally insured persons get. However, the EHIC is not as comprehensive as travel insurance. It does not cover private healthcare, repatriation costs, lost or stolen property, emergency transport, or a wide range of other non-medical travel losses.

Personal Liability Insurance

Personal liability insurance is one of the insurances that is common as a separate insurance in some countries, uncommon in some, and means different things in different regions. In some countries it is a very important stand-alone insurance, whereas in some countries it is frequently bundled into household cover rather than purchased as a separate product.

In France, for instance, personal liability included in your household insurance provide coverage for damage caused to third parties by the insured, family members, animals, and objects under the insured’s custody. A typical example would be a child that breaks another child’s glasses or a dog who bites a random pedestrian.

In spite of being a neighboring country to France, Germany has a very different system with respect to personal liability. In Germany, personal liability insurance is treated as a stand-alone core insurance product and is considered one of the most important insurances to have.

The conclusion to be drawn here is that the practical significance of personal liability insurance depends on how a national market allocates everyday private-life risks between tort law, mandatory housing-related cover, and voluntary household insurance.

Private Health Insurance

Another insurance type that differs substantially within the EU is the private health insurance. OECD data shows that private health insurance and how it works is largely dependent upon the national financing model.

In the Netherlands and Switzerland, private health insurance is of fundamental importance to the healthcare system. In Germany it is the primary cover for citizens who have opted out of social health insurance. Conversely, in countries such as Sweden, Estonia, and the Czech Republic, private health insurance is comparatively small in spending terms. OECD estimates indicate that private health insurance accounts for around 60% of health spending in the Netherlands, nearly half in Switzerland, but 5% or less in around half of OECD countries, and is almost non-existent in Sweden.

Accordingly, you can’t answer the question of whether private health insurance is something you need or something that is worth it, without first answering the question of which country’s health care system you are dependent upon. In one country the product may primarily buy faster access or broader provider choice while it in another functions as the primary access to health care.

Income and Accident Protection

Income and accident protection is a particularly complex issue to analyze from an insurance perspective. Relevant protection may be found in several different places based on how your personal situation looks and which country you live in. According to MISSOC, protection can be found in statutory social-security systems, employer-paid sick pay arrangements, collectively negotiated benefits, and privately purchased insurance products.

As a result, the central consumer problem is often not the complete absence of protection, but uncertainty as to which mechanism responds, under what conditions, and to what extent.

Income-replacement and accident-related protection sit at the intersection of public systems and private insurance markets, which means that both overlap and residual exposure are common. A consumer may therefore appear protected on paper while still facing material gaps in waiting periods, eligibility conditions, benefit duration, occupational scope, or compensation thresholds.

Also, products that appear to insure the same risk may do so in fundamentally different ways. Under the Solvency II classification, accident and sickness insurance may be structured as fixed pecuniary benefits, indemnity-based benefits, or combinations of the two.

Hidden Coverage You Might Not Know You Have

Payment Card Insurance

One hidden coverage that you might have is insurance protection through your credit card. Some credit cards offer purchase protection, where an item bought with the card can be covered for loss or damage for a certain period after purchase (often 90 days). Another even more common type of insurance is the travel insurance. However, the travel insurance is typically subject to tough restrictions. According to official EU consumer guidelines, these insurance generally require meeting specified criteria. The most classical criteria is that you need to have paid for the relevant travel using the eligible card to 50%, 75% or sometimes even up to 100%, in order for the card’s travel insurance to apply.

The typical consumer question “am I covered through my card” can't be answered on a stand-alone basis. It needs to be followed by approximately a dozen additional questions. Covered for what? Paid with what? Eligible travelers? Covers cancellations? Covers medical emergencies?

Employer or Union/Membership-based Cover

Many European consumers have some form of insurance protection they might or might not know about through their employment or union membership. In some instances, these protections are considerable. In other instances, they provide little to no value at all.

In Sweden for instance, the clearly most common type of insurance offered by the Swedish employment unions is the income insurance, which tops up the public unemployment system compensation (A-kassa) if you would lose your job. Other insurances that unions often provide to their members are group life insurances, personal accident insurances and certain forms of medical insurances. You should always familiarize yourself with the insurance offerings your union gives you if/when you become a member.

How to Read an Insurance Policy Without Getting Lost

Start with Exclusions, Not Promises

Consumers instinctively begin reading the generous portion of the document. They review sections labeled “what we cover” and proceed onward. This behavior is understandable and it’s also what the insurance companies want you to do. Unfortunately, it is also the wrong way to determine whether a claim will ultimately be paid or not.

Our advice here is to start with reading all exclusions. Various conditions, territorial limitations, causation language, maintenance responsibilities, security requirements, waiting periods – the list goes on. These exclusions and other limitation language is a better starting point when trying to understand what you’re actually covered for.

You Might Be Protected But Still Get Nothing

Let’s say that you’ve lost an old electronic device. It was initially worth 400 EUR You have had it for 3 years and with your particular insurance, the age reductions are 25% a year. The payout for this loss would then be 100 EUR. However, your deductible for lost electronics is 120 EUR. This means that in this specific scenario, you are protected, but the protection is useless.

Definitions might have a similar excluding effect. Who qualifies as an insured person? What constitutes theft? Was an item attended? Is an event sudden or accidental? What constitutes a covered trip? What constitutes permanent disability?

Additional concepts consumers rarely track well include: notification time frames, valuation methods, proof requirements, territorial scope, obligations to mitigate losses, exclusionary provisions for wear and tear, and specialized limits for high-value items. All of these things can be detrimental to your claim and it is much better to know of them before something happens, than when after something has already happened.

Contract Summaries and Product Pages Don’t Give You The Full Picture

Most people do not read full insurance contracts. And that’s very understandable. Lucky for them, they no longer have to with the entrance of InsurAGI on the market!

But the real trouble is not that consumers don’t read the full terms and conditions of their insurances. It’s what they read instead. Product pages, summary tables, and onboarding messages are all helpful information, but it is not sufficient as anything else than orientations.

What summaries specifically cannot do is resolve difficult situations. When losses are simple, broad summaries can provide reasonably accurate representations. When losses involve significant costs or unusual circumstances, you need the full terms and conditions to get a correct answer.

The Biggest Mistakes People Make When Comparing Insurance Across Borders

To compare insurance across borders, consumers typically must overcome four obstacles:

-

Finding the right comparisons. You can’t only compare insurance premiums and insurance types. The comparison must also include the relevant exclusions in both insurance policies and the legal context of the insurance.

-

Comparing “like” words instead of “like” functions. Home insurance policies in Sweden and home insurance policies in Germany are vastly different from each other. Look at whether or not the compared insurances include coverage for contents, liability, legal assistance, and travel extensions. The mere fact that both insurances have the same title does not – really – mean anything at all.

-

Failing to consider the public-private split. Before you as a consumer can decide whether a private insurance product is “good value”, you must determine what public protection (state, employer or statutory system) it lies on top of. The same private coverage in two different states can give entirely different outcomes due to the underlying public coverage.

-

Placing too much reliance on distributors’ summaries. Cross-border consumers are susceptible to misunderstandings from overly simplistic summaries. You can’t focus solely on IPIDs or summaries, the real extent of the protection is in the full terms and conditions. InsurAGI’s AI-assistant can help you interpret the terms and conditions and help you avoid financial disaster that might otherwise follow in a situation like the below.

How Households Can Build a Smarter Insurance Portfolio

Households do not need to become professors in insurance. They just need a better process. The below 5 steps should be a useful starting point.

-

Start with exposures, not products. Which financial losses would potentially impact this household? Just because another household has insurance product A doesn’t mean you should too. They might have an entirely different exposure. Beginning with exposures maintains the household’s framework and is a much better starting point.

-

Map all existing layers before acquiring new products. Before getting new insurance, spend some time understanding exactly what coverage you already have. To find hidden coverage, you can use InsurAGI. Hidden coverage could consist of private retail policies, employer benefits, union coverage and card-linked insurance. Most people acquire insurance too quickly, solving perceived uncertainty rather than first verifying a gap in their coverage.

-

Categorize into three columns. Try to categorize your insurances into the following three groups: probably essential, context-dependent and likely duplicative.

-

Review one level deeper than you want to. Examine exclusions, definitions, deductibles, territorial limitations, co-insurance, notification procedures, high-value item limits and cancellation triggers. They ALL matter.

-

Review your insurance setup every time your life setup changes. Life can change a lot. Moving, having children, changing jobs, divorce, purchasing large items, traveling extensively, remote working abroad, it is unlikely that your life continues as it looks when you’re reading this forever. As life changes, your insurance assumptions may become outdated faster than you anticipate.

That is a more durable way to think about insurance in Europe. It is more elegant than simply asking for the “best policy”, and much closer to how sensible protection is actually built.

Summary: What Newcomers to Some of The European Insurance Markets Should Notice First

A convenient way to assess variations in European insurance markets is not to inquire which country is best overall. Rather, the better inquiry is: if you are just beginning to arrive in this market, what should you notice first?

In Sweden: Notice how much protection there is in the standard household insurance (hemförsäkring). It is also a very common form of insurance among Swedes, seeing as housing associations and landlords normally require the owner/tenant to have home insurance. Swedish home insurance often functions as a sort of umbrella insurance, with lots of different protection components in it. This makes it more comprehensive than a typical home insurance product in other parts of Europe.

In Denmark and Norway: Notice both the resemblance to Sweden and the limits of that comparison. Both Denmark and Norway are – like Sweden - institutionally strong markets that consumers have a high trust in, but the bundled function of a Norwegian or Danish home insurance is not exactly as comprehensive as that in Sweden.

In France: Notice the degree to which insurance in France is legally required to some respects. Tenants need to have home insurance that cover fire, water damages, explosion etc. Someone new to insurance in France should therefore identify what insurance they must have according to the law, and what optional insurance coverage that might just be useful.

In Germany: Notice how Germany is a highly structured retail insurance market in which private personal liability insurance, among other products, is a normal and necessary part of reasonable private insurance protection. Someone new to insurance in Germany should focus less on the legal absolute minimum insurance levels, and more on what insurance protection that the market expects a bonus pater familias to have.

In the Netherlands: Notice that the insurance market is centered around the health system to a much greater extent than in other European countries. A prospective Dutch insurance holder should therefore begin with choosing a solid health insurance coverage and then plan from there.

In Spain: Notice that the most typical insurance in Spain is connected to what the banks require in order to give you a mortgage, i.e. mortgage-linked insurance. That is the main building block of any average Spanish insurance holder, with other private insurance on top of it. Pay close attention to how mortage-linked insurance, private insurance and public-backed mechanisms (from Consorcio de Compensación de Seguros) interact with each other.

In Italy: Notice how compulsory motor insurance, and not the typical home insurance, is the main insurance Italians focus on. This is partly a cultural phenomenon driven by the fact that Italian individuals above the age of 18 tend to leave their family home later than in Northern Europe and thus be covered by their parents’ home insurance plan. A newcomer should thus avoid assuming that home, family liability, or catastrophe cover is in the center of all insurance planning as it is in the Nordics.

In Ireland: Notice how Irish insurance can initially seem quite straightforward, but that waiting periods, pre-existing-condition rules, and mortgage-related protection play a significant role in how cover functions in practice. The system is public coverage with private coveage top-ups.

In Poland: Notice how compulsory insurance is concentrated in specific areas such as motor and agricultural risks. Private health insurance is growing but is much less common than in many other European markets. A newcomer should therefore avoid importing assumptions from Western European household-insurance culture and instead rebuild expectations from the Polish structure itself.

Conclusion: Understanding Your Landscape Is Helpful, Reading Wording Is Decisive

There is no single European insurance regime from a consumer’s viewpoint. Instead, what we have is a collection of overlapping markets that might resemble each other but that have great differences. Legal structures vary, access to health care varies, and how far you come with only public protection structures vary greatly too.

Broad comparative studies like this one are beneficial because they prevent individuals from incorrectly assuming that how it works in European Country 1 also reflects how it works in European Country 2.

However, comparative studies do not resolve claims. The definitive answer to “am I covered?” is based on the actual terms and conditions and the details of each incident. Definition of insured event, identity of parties covered, territorial provisions, deductibles and sublimits, requirements for proof of entitlement, timing requirements for filing claims, interaction among potentially multiple layers of coverage, are only a few of the relevant factors.

Luckily for you, we got you. Just use the InsurAGI AI-assistant to get perfect clarity as to your coverage and if a certain incident entitles you to compensation from your insurance or not.